Performance-Based Regulation: The Incomplete Fix and What Should Come Next

Post 2 of 10: The Potential Structural Transformation of the U.S. Electric Utility Industry

Ask a lineman what matters in his job, and he will tell you: keep the lights on, get them back on fast when they go out, go home safe. They work through hurricanes and heat waves and ice storms. The grid they maintain is the foundation that society sits on.

Ask the CFO at that same utility what matters, and you get a very different answer: deploy capital, earn a return on it, repeat.

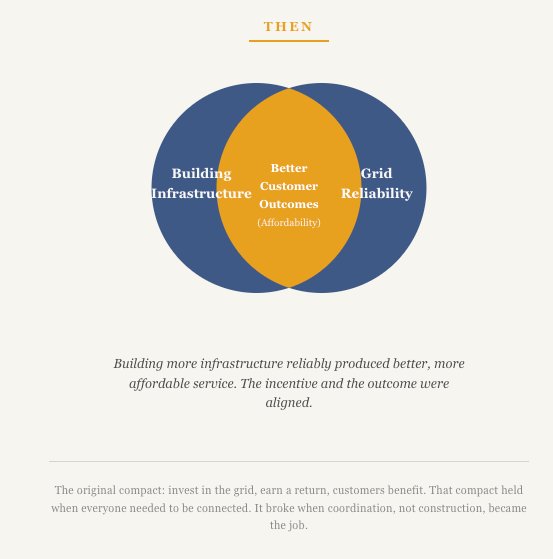

Cost-of-service regulation was designed about a hundred years ago for a clear purpose: connect everyone to the grid by building more infrastructure. The incentive made sense because people did not have electricity. Return on equity was a reasonable proxy for that, a way of saying: invest in building out the system and we will make sure you earn a return.

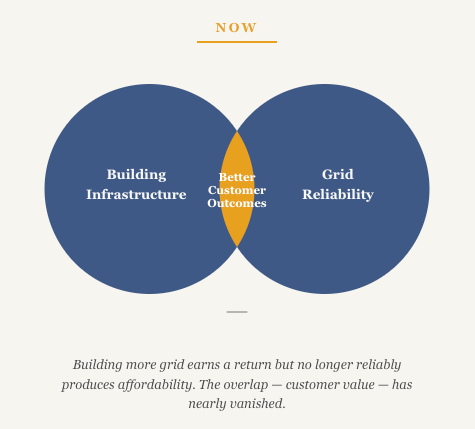

Now that everyone is connected, the incentive has outlived its original purpose. We are still using Return on Equity as an indirect way of paying utilities to deliver reliable, affordable power. This is the original sin and it is a terrible proxy. We should instead be paying them directly for achieving exactly what we want.

As I wrote in my last post, the compact between utilities and the public is breaking down because building more grid is not what is needed: coordinating the network is. But incentives matter. Performance-Based Regulation was the most serious attempt to change them. It was imperfect, and we should make it better.

In this note I will share thoughts on Performance-Based Regulation. In my next post, I will share how it can unlock a low-cost and abundant grid, even for data centers.

Hawaii: The PIM Scale Problem

Hawaii went first. Under then-Chair Jay Griffin, the Hawaii Public Utilities Commission ran a three-year stakeholder process and in December 2020 approved a PBR framework for Hawaiian Electric under Docket No. 2018-0088, the first of its kind for a U.S. investor-owned utility.

Credit to Jay and his team: being first is genuinely hard, and the political capital required to move that through a contentious process should not be underestimated.

However, the PIMs were not successful. Hawaiian Electric did not achieve a single meaningful one. Here is why that was predictable from the start.

Between 2020 and 2023, Hawaiian Electric’s consolidated average rate base grew by approximately $392 million (from $3.48 billion to $3.87 billion). At the authorized 9.5% ROE and a 56% equity ratio, that capital expansion generates roughly $21 million in new annual authorized net income, though the utility’s persistent under-earning (consolidated book ROE of 8.2% in 2023) means the actual incremental earnings were likely closer to $18 million. These earnings are continuous for the 20 to 40 year life of the assets.

Now compare that to the one-time PIMs sitting alongside it:

Interconnection Approval PIM: capped at approximately $3 million annually across all operating companies. Collective Shared Savings Mechanism: capped at $5 million for Oahu and $1 million for neighbor islands. HECO generated $0 from this in 2023 because expenditures exceeded the base year targets. RPS-A PIM: capped at $20 per MWh of accelerated renewable generation, yielding a few million dollars depending on third-party project timelines.

Achieving maximum PIM payouts requires flawless execution against escalating targets for a one-time bonus typically yielding $1 to $3 million.

Deploying a standard $50 million grid modernization project guarantees an equivalent baseline return at exponentially lower operational risk, with a continuous yield over the asset’s lifecycle.

PIMs did not change the incentive. They placed a small one-time prize next to a large continuous one and hoped the large continuous one gets ignored. It did not. The PIMs operated at the margin of utility earnings while capital deployment remained the dominant revenue driver.

But there is a second failure in Hawaii that gets less attention: the accounting problem.

When a utility transitions from traditional cost-of-service to a PBR framework, it creates significant complexity under ASC 980, the U.S. GAAP standard governing regulated operations. Regulatory assets established under the prior framework interact with PBR mechanisms in ways that introduce financial statement volatility that was not present under traditional regulation. The recognition of PIM revenues, the treatment of deferred costs, and the valuation of regulatory assets in a PBR environment all become contested. For bond investors and credit agencies, this uncertainty raises the cost of capital at the exact moment a regulator is trying to reduce rates. It is a structural friction that no state has cleanly solved.

There are thoughtful financial structuring approaches that can address this. I will not go into the details here as they are technical, but if you are serious about solving this problem at scale and want to discuss it further, send me a message and I can share some solutions.

Connecticut: What Happens When Reform Gets Adversarial

Connecticut tried a more direct approach. PURA Chair Marissa Gillett proposed compressing ROE toward actual cost of equity, which is the right instinct: utilities have long earned authorized returns that exceed market requirements, which is why they trade up to 2x their book value.

Eversource responded in May 2024 by announcing it would cut $500 million in Connecticut capex over five years and redirect investment to Massachusetts and New Hampshire. Both Eversource and Avangrid filed lawsuits alleging regulatory bias. S&P downgraded Connecticut utility credit ratings in December 2024. Marissa Gillett resigned as PURA chair effective October 2025. The board was reconstituted. The utilities ran out the clock.

I believe that Gillett had the legal architecture to withstand the challenge. The Hope and Bluefield standards, which govern what constitutes confiscatory ratemaking under constitutional review, were not violated by her approach. What she did not have was the political durability to survive a sustained multi-year campaign of litigation, capital reallocation threats, and lobbying. The utilities did not need to win in court. They only needed to outlast her while lobbying politicians. And they did.

The full playbook, run over roughly three years: capital reallocation threats implying service degradation if returns compress, simultaneous litigation from two utilities designed to create regulatory paralysis, credit agency pressure through selective communication, and sustained lobbying to reshape the political environment around the commission. Every tool was deployed in sequence until the regulator was gone.

That is not a Connecticut problem. That is the utility playbook. It will be run again wherever a regulator gets close to the underlying ROE question.

Is Totex Part of the Answer?

The UK’s Totex model gets cited constantly as a solution. In this framework, regulators set an ex-ante allowance combining capex and opex, applying a uniform capitalization rate to both. It deserves credit for identifying the capex bias: utilities structurally prefer to build rather than operate smarter because they only earn returns on capitalized physical assets. Totex tries to neutralize that by pooling the two. But the Totex solution has some non-obvious flaws.

First, the goal is still fundamentally about budgeting. Inflate the forecast, inflate the baseline. Regulators are not equipped to audit utility forecasts with operational granularity, and this creates a new front for bloated allowances that are hard to challenge. Unintuitively, we may actually want utilities to increase opex and capex adhoc if they think it will drive down total costs in the long run - the Totex system doesn’t fully account for this.

Second, it still does not orient payment toward outcomes. Vendors pitch their solution as a cure-all. You sign a ten-year enterprise software contract categorized under Totex. If that software fails to deliver proportional grid efficiency, the expenditure is already locked into the regulatory allowance. No wonder software vendors are the biggest champions of this model.

The utility earns its return on that authorized spend regardless of whether the solution actually worked. The alignment problem, does this actually help customers, is not fixed.

After thirteen years of RIIO rounds, Ofgem cut 26% from what UK utilities requested in RIIO-3 baseline expenditure. A system requiring the regulator to forcibly slash a quarter of the proposed budget is not a framework working smoothly.

What I Think Needs to Happen: Move to Market-Based ROE and Pay for Outcomes

Every state that has attempted PBR has tried to fix the incentive while leaving the underlying ROE structure in place. That is the wrong sequence. Here is what I think the right sequence looks like.

Step one: set a market-based ROE. A regulated monopoly with guaranteed cost recovery should earn a return that reflects actual market requirements. At a true market-based ROE, utilities will still attract capital and still build what is needed. They just will not earn excess returns for doing it. Connecticut was trying to get here. The goal was right.

To preempt constitutional challenges under the Takings Clause regarding confiscatory ratemaking, regulators can satisfy the Hope and Bluefield standards through direct market-clearing mechanisms. Utilizing competitive bidding for project-level equity replaces proxy models with actual market data, inherently proving capital attraction and comparable earnings under the end result doctrine.

Step two: structure the traditional CAPM-derived ROE as a put option. The utility must first bid out new capex equity to the market. If the market fails to clear below the regulatory strike price, the utility deploys corporate capital at the approved CAPM rate, just as they do in today’s status quo. But the difference is they should only do so if no cheaper capital can be found. This structurally guarantees capital availability while capturing pricing efficiencies when the market clears lower.

Step three: once the ROE baseline is set at market cost of capital, explicitly pay for the outcomes customers want. Align these payments to the Regulatory Trilemma: reliability, affordability, and sustainability. The weight of that third goal varies by state, but the first two are universal. Set clear KPIs for each. Design good, better, best payout tiers so the utility knows exactly what it earns for each level of performance. Then step back and let the utility decide how to achieve those outcomes. Do not specify the inputs. Reward the outputs. The utility knows its system better than the regulator does. Give it the room and the incentive to use that knowledge.

This payment should be in dollars, not in basis points on a rate base. If a utility cuts customer costs by $50 million, pay it a direct share of that savings. That is what finally aligns the lineman’s instincts with the financial model. Under cost-of-service, the utility earns more by spending more. Under this framework, it earns more by delivering better value to customers.

This model already exists in a limited form. LIPA, the public authority that owns the Long Island grid, contracts with PSEG Long Island to operate it under a management services agreement. A meaningful share of PSEG Long Island’s annual compensation, roughly $23 million at risk in 2024, is tied to performance metrics across reliability, customer satisfaction, and clean energy delivery. PSEG Long Island earned 67% of available variable compensation in 2024.

The Trust Problem and the Information Gap

This framework requires something that is currently in short supply: trust. As I wrote in my first post, utilities principally sell trust. They happen to also sell electricity and build infrastructure, but trust is the product. Right now that trust is low on both sides. Regulators and stakeholders do not believe utility cost projections. Utilities feel like everyone is against them.

Part of why trust has eroded is structural information asymmetry. Utilities know their system better than anyone. Regulators, intervenors, and ratepayers have limited ability to independently verify what utilities tell them about costs, asset conditions, or project necessity.

The prudency review standard evaluates whether an investment decision was reasonable at the time it was made - but few outside of the utility have the data to audit. The current process does not require post-investment reporting on whether the asset was actually needed or actually used. There is no mandatory utilization reporting for rate-based capital projects. Once an asset clears the prudency review and enters rate base, it earns a return for its full depreciable life regardless of how often it is dispatched or whether the problem it was built to solve ever materialized.

Building trust requires changing this. Outcome-based frameworks only work if both sides can verify the outcomes and understand the inputs. That requires real-time data sharing, independent technical review, and post-investment auditing that does not currently exist in most jurisdictions.

The New Operating Model

This framework requires not just regulatory redesign. It requires a fundamentally different kind of utility operator.

The lineman and the field crews do not need to change. They already know how to do their job. Their north star, keep the lights on, get them back on fast, go home safe, is exactly right. It is the management layer and the incentives above them that needs to be rebuilt around the same clarity of purpose.

A utility optimized for outcome delivery looks different from a utility optimized for capital deployment. Its planning process explicitly seeks to avoid capital investment where a cheaper solution exists. It builds minimum viable pilots before committing to full system rollout. It is constantly iterating and deploying. It tracks utilization rates on every major asset. It measures success in customer outcomes, not in capital spent or projects completed. It treats operations as a core competency rather than a pass through cost center.

The culture has to match the incentive. Right now the incentive rewards building. The culture that grew up around that incentive rewards certainty, process, and scale. Replacing it with a culture that rewards rapid iteration, outcome measurement, and operational creativity requires real leadership at the top of the organization. It also requires different skills and tools in the building. The people best at navigating rate cases are not always the same people best at running operationally excellent service businesses. Both matter. But the balance shifts when the financial model shifts.

The incentive structure has to come first. You cannot build a modern grid on a hundred-year-old business model. But changing the incentive without changing the culture, the processes, and the purpose of the organization is just drawing a new org chart on top of an old one. The two have to move together.

That is the harder part. It’s real leadership. And it is the subject of several posts ahead in this series.

In my next post, I will show how paying explicitly for the outcomes society wants creates abundance, reliability, and low cost on the grid when we need to rapidly build out for data centers.

Utility Transformation Series, Post 2 of 10 Next: How PBR unlocks an affordable and reliable grid that is aligned to speed-to-market.

Sources

Hawaii PUC, Docket No. 2018-0088, PBR Framework Decision (December 2020)

Hawaii PUC, Overview of the PBR Framework, puc.hawaii.gov

HEI Statistical Supplement and annual filings (2020-2023)

Eversource Q1 2024 Earnings Call

S&P Global, credit rating actions on Connecticut utilities (December 6 and 10, 2024)

CT Mirror, “Marissa Gillett to resign as PURA chair” (September 19, 2025)

Ofgem, RIIO-3 Draft Determinations

Utility Dive, “Hawaii finalizes utility regulation considered potential template” (January 2021)

LIPA, 2024 Year-End Report on PSEG Long Island Performance Metrics (June 2025)

Werner and Jarvis, “Rate of Return Regulation Revisited,” Energy Institute Working Paper 329, UC Berkeley (2022)

Assumption note: Rate base growth and ROE figures for HECO use the authorized 9.5% ROE and 56% equity ratio from the PBR framework filing. Asset growth figures derived from HEI consolidated balance sheets. PIM cap figures sourced from HPUC annual PIM reporting under Docket No. 2018-0088.